Sponsored by

(Support Wealth Potion by visiting our sponsor^)

Imagine your salary went up 5%. You'd be happy, right?

But what if inflation was 6%?

Bad news: You are mathematically poorer than you were a year ago.

Welcome to the lived reality for millions of people over the past few years.

This compares wages to CPI, which we’ll challenge in just a moment.

Wages have been rising fast enough to feel like progress, but not fast enough to stay ahead of the purchasing power drain of inflation. Real wages have been flat.

And I know what astute readers may be thinking…

"Nice try, Brandon... the most recent CPI print was 2.5%!"

Yes, you are correct.

But firstly, inflation is cumulative… and CPI has been averaging ~4% over the past 5 years.

And worse yet, the way that CPI is measured -- which is intended to measure the cost of living -- has been altered in recent history to reduce the impact of volatility in housing prices.

Here's a riddle for you:

What is your biggest expense as it relates to your cost of living?

(Hint: it's something that young people are struggling to afford...)

You guessed it: Housing.

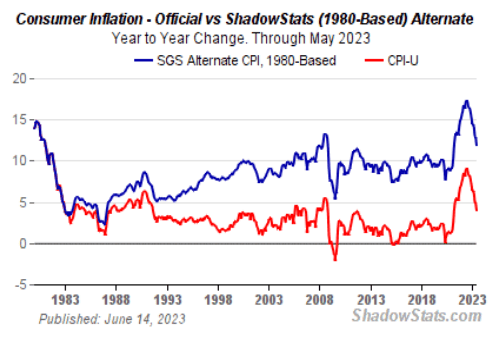

And if we use the CPI methodology from 1980 -- before it was adjusted to reduce the impact of house prices -- then annual inflation has been closer to 10-15%.

The 1980 “CPI” would show inflation at 10-15%

tl;dr - The low-inflation world that we were promised no longer exists.

And to build wealth in high inflation times, you need a different playbook.

Today’s article is everything you need to know about building wealth in high inflation times.

Let’s dive in.

Something Big is Coming…

I have a very exciting announcement coming soon and I want you, my long-time supportive reader, to be the first to know.

Here’s a sneak peek:

More than that, I want to reciprocate your love and support for Wealth Potion.

Newsletter subscribers will be getting the early-scoop before I go live (along with the ability to lock in the best discount I will ever offer). So stay tuned!

Think of it as a sincere ‘Thank You’ for your support and encouragement these past few years 💖

Now back to the article.

The Standard Wealth Model Is Broken

"Save more. Spend less. A dollar saved is a dollar earned."

Solid advice. But with a caveat.

That advice works best when inflation is 2%. At that rate, a savings account paying 0.5% only loses you ~1.5% per year in real terms. Which is painful, but manageable.

At 5% inflation, the math becomes brutal. You’re now losing 4.5% of your purchasing power per year.

At an 8% inflation rate, every dollar sitting in a checking account loses roughly 33% of its purchasing power in five years.

You think you’re saving money, but in reality you're donating to whoever owns the assets you're not buying.

At Wealth Potion, we often tell you that you need to own assets. High inflation only makes this even more imperative. Cash is a melting ice cube, and inflation makes it melt faster.

Inflation is a wealth transfer. It moves value from people who hold cash to people who hold assets. If you're not in assets, you're on the wrong side of that transfer every single day.

Why Inflation Punishes Savers Hardest

Inflation doesn't hit everyone equally.

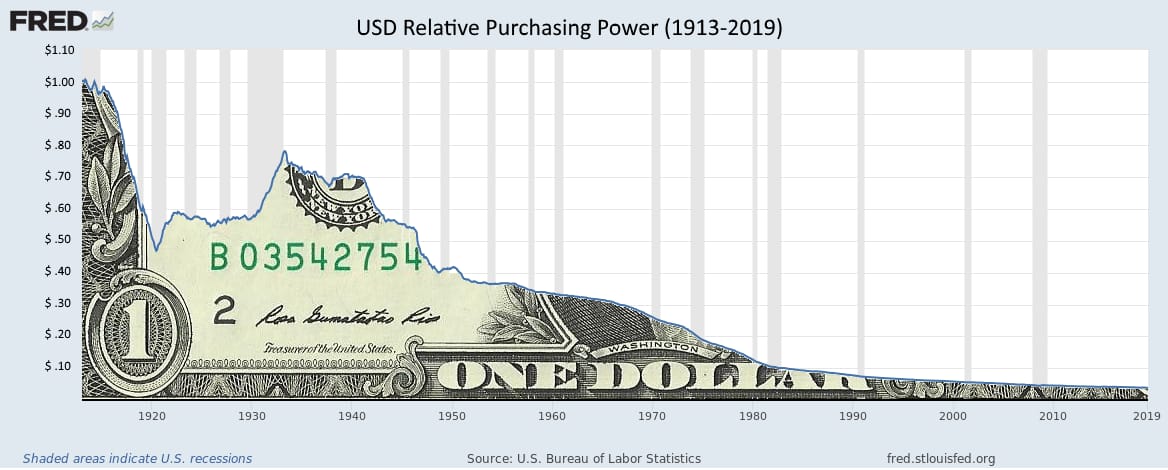

It hits people who hold money in dollars (or any fiat currency) the hardest. Their savings get diluted.

Meanwhile, anyone holding real assets -- stocks, real estate, commodities, Bitcoin -- sees those asset prices inflate alongside everything else.

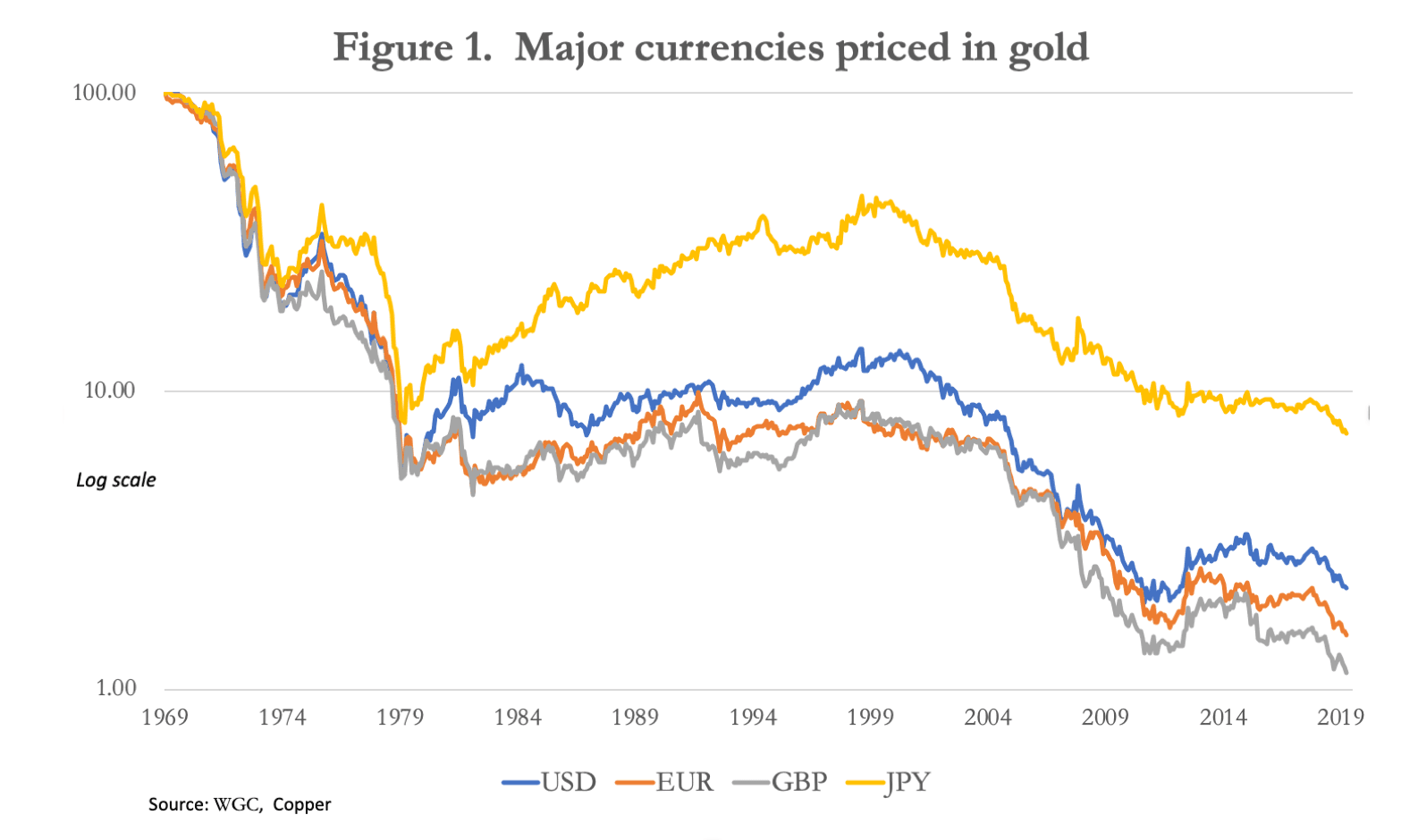

As a Canadian, many of my friends and family have asked over the years "Should I be buying U.S. dollars instead? Is that safer than Canadian dollars?"

And the answer oftentimes is "technically, yes". The U.S. dollar is, generally speaking, safer than other fiat currencies. But it is still a fiat currency. It is still subject to inflation.

The U.S. dollar is the most eligible bachelor at the leper colony. So trading your Canadian dollars (or any other fiat) for U.S. dollars is kind of like shuffling around chairs on the Titanic.

This is why the same economic environment that crushes middle-class savers tends to make wealthy people wealthier. It's not that the rich are smarter. It's that they're holding different things.

The path to building wealth during high inflation isn't to save more dollars. It's to hold fewer dollars and more assets.

What Will Your Retirement Look Like?

Retirement looks different for everyone. What it costs, where the income comes from, how long it needs to last. Those answers are specific to you.

The Definitive Guide to Retirement Income helps investors with $1,000,000 or more work through the questions that matter and build a plan around the answers.

Download your free guide to start turning a savings number into an actual retirement income strategy.

The Inflation-Aware Wealth Framework

The framework has three pillars:

Where your money is stored,

How much of it leaks out to lifestyle creep, and

What you're actually building toward

Assets Over Cash. Always, But Especially Now.

In a low-inflation environment, keeping a year of expenses in cash is a reasonable buffer.

In a high-inflation environment, anything beyond three to six months of emergency reserves is likely damaging your portfolio unnecessarily.

Index ETFs are your baseline. A broad-market index fund gives you ownership in hundreds of companies whose revenues, assets, and earnings adjust (imperfectly, but directionally) with inflation over time. Dollar-cost averaging into index funds is one of the most reliable inflation defenses available to ordinary people.

Bitcoin deserves a separate conversation. Unlike equities, which represent fractional ownership of companies that can dilute or underperform, Bitcoin has a fixed supply cap of 21 million coins. No central bank can print more of it. No government can expand the supply to cover spending. Bitcoin’s absolute scarcity is what makes it a fundamentally different kind of asset in an inflationary environment.

The problem with conventional currency is all the trust that’s required to make it work. The central bank must be trusted not to debase the currency, but the history of fiat currencies is full of breaches of that trust.

The question "is Bitcoin an inflation hedge?" doesn't have a clean short-term answer. Prices are volatile. But over longer timeframes, the logic is sound: a fixed-supply asset in a world of infinite supply expansion tends to win. Size your position according to your risk tolerance, buy consistently, and think in years (or decades).

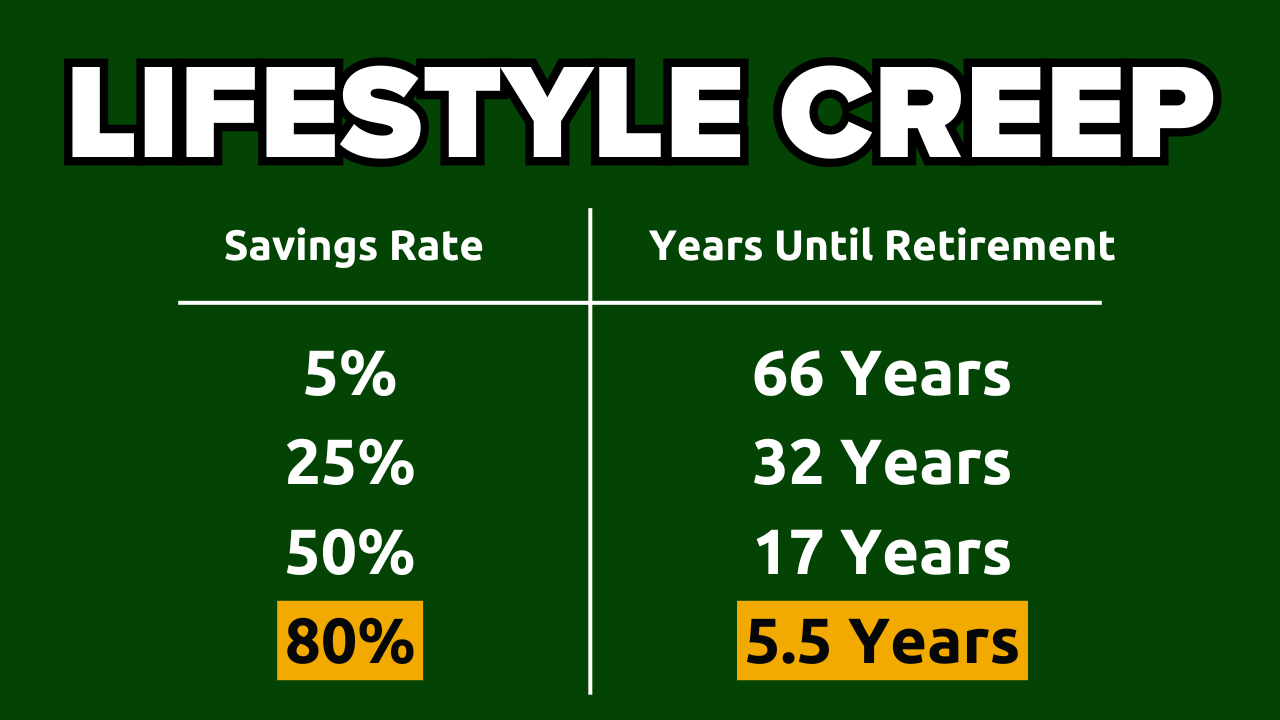

Cut Lifestyle Creep Before Inflation Does It For You

Inflation and lifestyle creep are a brutal combination.

As prices rise, your spending naturally drifts upward. Restaurants cost more, rent increases, subscription services raise their prices. And when your income increases, you feel richer, so you often add more to expenses to your plate - unaware that your existing expenses are already inflating.

The result = your cost of living scales faster than your income, even as you nominally earn more. You feel busier, more stretched, and no closer to financial independence.

Lifestyle creep is one of those silent destroyers of wealth-building momentum, and high inflation makes it worse because the spending drift is partly hidden by rising prices. You can't always tell whether you're spending more because you're living better or because everything costs more.

The fix must be deliberate. Audit your recurring expenses quarterly. Treat your investment contribution as a fixed cost, not an optional one.

Build a Wealth Formula That Inflation Can't Erode

The simple formula for building wealth holds in any environment: income minus spending equals capital to deploy. But high inflation squeezes both sides. Inflation cuts the real purchasing power of your income and inflates your cost of living.

Which means you need to actively manage both sides, and not let them drift:

On the income side: inflation is the strongest argument for asking for a raise, that applies to literally everyone. Your employer's revenues are probably inflating; your real wages shouldn't be absorbing the gap.

On the spending side: direct every freed-up dollar into assets before inflation turns it into a less valuable dollar. Remember… melting ice cube.

The goal is a high savings rate converted immediately into inflation-resistant assets. Cash is a temporary holding zone, not a destination.

Practical Steps to Build Wealth in High Inflation Times

1. Audit your cash position today. Anything beyond a 3-6 month emergency fund sitting in a low-yield account is losing real value. Make a plan to deploy the excess into index ETFs or Bitcoin. Gradually if needed, but start.

2. Set a DCA schedule and automate it. Dollar-cost averaging takes emotion out of volatile and frantic markets. Set a recurring buy into your chosen assets (weekly, monthly, or even daily) so you're deploying capital regardless of whether prices are up or down.

3. Comb through your subscriptions and recurring expenses. Not to deprive yourself, but to distinguish deliberate spending from automatic spending. High inflation is a reasonable prompt to renegotiate, cancel, or downgrade anything that crept in without a conscious decision.

And those subscription prices are always increasing over time because of… you guessed it: inflation.

4. Make your next raise work harder than the last one. When you receive a pay increase, decide in advance what percentage goes straight to investments before you see it in your account. This is the “pay yourself first” model and many people swear by it. It might work for you too.

5. Add Bitcoin to your portfolio, sized proportionally. This is not financial advice, but even a small allocation to a fixed-supply, globally accessible asset provides inflation diversification that equities alone don't offer. Buy only what you understand, hold it properly, and don't sell during volatility. If Bitcoin still freaks you out, look into gold.

FAQ

Isn't Bitcoin too volatile to be an inflation hedge?

In the short term, yes. Bitcoin can move 30-50% in either direction. But inflation hedging is a long-game thesis. The relevant question is whether a fixed-supply asset holds purchasing power over a decade. The data so far suggests it does. Size your position so that short-term volatility doesn't force you to sell at the wrong time. As I’ve shared in the past, I am irresponsibly long Bitcoin. DYOR.

What if I genuinely can't afford to invest right now?

That's the right question to ask, but usually the wrong conclusion. In most cases there are discretionary expenses that can be redirected, but they’ve become invisible. Start with a spending audit before concluding there's nothing left to deploy. Even $50/month into an index ETF builds the habit and compounds meaningfully over time. And with fractional shares, you can start with as little as a $1 DCA.

Should I pay off debt or invest during high inflation?

Depends on the interest rate. High-interest debt (e.g. credit cards, payday loans) should almost always be cleared first. No investment reliably returns more than 20%+ consistently. Low-interest debt (e.g. mortgages, a HELOC, student loans below ~5%) is actually less painful in real terms during inflation because you're repaying with cheaper future dollars. In that case, investing in parallel makes sense. And debt can be a powerful form of leverage. But you know what they say about leverage…

If you're smart you don't need leverage; if you're dumb, it will ruin you.

Is real estate still a good inflation hedge?

Historically, yes. Both property values and rents tend to rise with inflation. But real estate is capital-intensive, illiquid, and comes with leverage risk when rates are high. Real estate tends to appear extra attractive because of the debt conundrum we mentioned above (inflation means you pay off debt with less-valuable dollars in the future). Index ETFs and Bitcoin are more accessible starting points for most people before adding property to the mix.

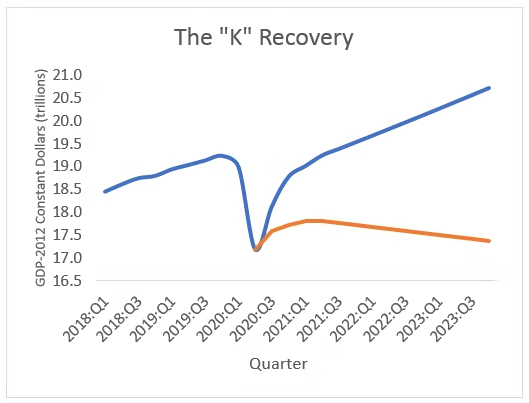

The Bottom Line

The wealth gap in an inflationary environment isn't primarily about income. It's about allocation.

It’s the have-assets vs. the have-nots.

People holding savings in cash watch purchasing power evaporate. People holding assets watch their portfolio reprice alongside the same inflation that's hurting everyone else.

The K-shaped economy. It was clearest in 2020, but it’s been happening ever since.

You don't need to be wealthy to get on the right side of that dynamic. You need to understand it and act on it. Which means owning assets, and not holding too much cash.

Want the full framework for navigating an inflationary economy? Join the Wealth Potion newsletter if you’re not already subscribed.

To your prosperity,

Brandon @ Wealth Potion